Foreclosures just hit a six-year high and while everyone claps for a steady mortgage rate the federal lifeline expires right on cue.

The number nobody's putting on the pretty graphic

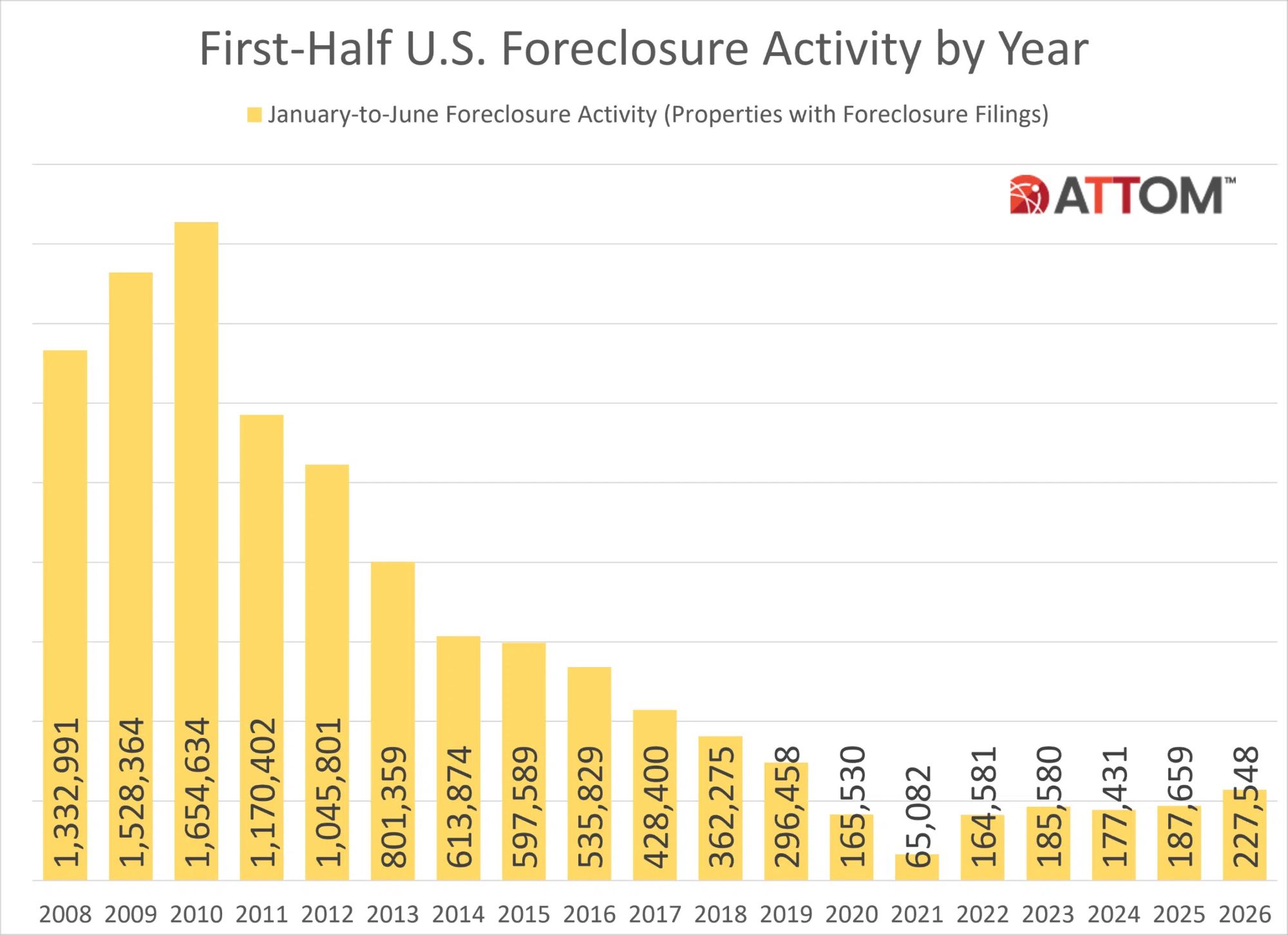

Here's the story hiding underneath the steady-rate headline. ATTOM just released its 2026 Mid-Year Foreclosure Market Report, right around the 14th, and the trend line is not cute. Foreclosure activity has now risen year-over-year for eleven-plus months straight — that's not a blip, that's a season. Q1 2026 filings came in up 26% from a year earlier. In May, 40,355 properties had a foreclosure filing, up 14% year-over-year. Foreclosure starts up 13%. Completed foreclosures — the REOs, the point of no return where a family actually loses the house — up 6%.

And the one that made me put my coffee down: foreclosure inventory is at a six-year high, per Cotality. Six years. We haven't seen this much distress sitting in the pipeline since before the world learned what "sourdough starter" meant. So while the market throws a little party because the rate didn't jump, there's a quiet, ugly parallel story where more and more households are getting the certified letter nobody wants.

Okay, breathe — this is NOT 2008

Now, I am a sass merchant, not a fear merchant, so let me be very precise, because precision is the whole job. This is not 2008. It's not the cliff. ATTOM itself frames overall foreclosure volumes as still well below historical norms. May was actually down 5% month-over-month. This isn't a crash where the floor drops out from under twelve million people in a weekend. It's a grind — a slow, steady, year-over-year climb higher. A dripping faucet, not a burst pipe.

But here's my problem with the "well below historical norms" crowd: that phrase is cold comfort to the actual human being whose name is on the filing. Averages don't pay mortgages. You can be a statistically-reassuring data point and still be losing your home. Both things are true at once, and grown-ups can hold both. The market is not collapsing. Real families are still hurting. Full stop.

The part that makes me want to throw something

Here's where I get spicy, and I'm punching at the policy, not the people. Right as this distress is climbing, a chunk of the federal relief lifeline — the FHA loss-mitigation and forbearance programs that have quietly kept a lot of people in their homes — is expiring. National Mortgage News is reporting that FHA relief-program expirations are already driving a surge in foreclosure-help calls. Read that again slowly. The safety net is being rolled up at the exact moment more people are falling toward it.

You do not have to be a bleeding heart to think that's dumb policy timing. You just have to own a calendar. Pulling the ladder up mid-climb is how you turn a manageable grind into a genuine mess. Ask who gets left holding the bag. It's rarely the people writing the press release.

Meanwhile, in Kansas City

Now the local silver lining, because I love this metro and I'm not going to doom-spiral you for clicks. The highest-foreclosure-rate states right now are Florida, South Carolina, Maryland, Nevada, and Indiana. Neither Missouri nor Kansas is anywhere in that top tier. So on a relative basis, the KC metro is holding up better than a lot of the country. Not immune — but better positioned.

And there's a second thing keeping our market weird in a stabilizing way: the rate-lock effect. Millions of owners are sitting on 3%-ish pandemic mortgages, and you could not pry those loans out of their cold, refinanced hands. Why trade 3% for 6.49%? You wouldn't. So they don't sell, inventory stays tight, and prices stay propped up even as distress ticks higher underneath. It's the strangest housing market I've worked in: not enough homes for sale, and a rising number of homes quietly heading toward foreclosure. Both. At the same time.

What this actually means for you

If you're a homeowner feeling the squeeze — behind a payment, dreading the mail, doing math at 2 a.m. — hear me: falling behind is not a moral failing, and it is not the end of the story. There are still options. Loan modifications, refinancing scenarios, a strategic sale with real equity before things go sideways, forbearance conversations while the door's still open. The worst move is silence, because silence is the one thing that guarantees the bank writes the ending for you. The FHA window closing makes acting early more important, not less.

If you're a buyer or an investor, let's be honest with each other: a rising tide of distressed inventory is, bluntly, an opportunity. More motivated sellers, more short sales, more eventual REOs mean deals for people with cash and patience. But it's a bittersweet opportunity, and I'd rather you buy with your eyes open and some decency in your chest than treat somebody's worst year as a clearance rack.

That's the whole JANAINKC promise: I'll tell you the truth the headlines won't, and then I'll actually help you do something with it. So — which one are you? Stressed owner who needs options before that FHA window slams shut? Message me and we'll map the exits together, quietly and with zero judgment. Buyer or investor eyeing distressed deals across the KC metro — Johnson, Wyandotte, Jackson, Clay, Platte? Let's build you a game plan before the crowd figures out what the steady-rate headline was hiding. Either way: I read the fine print so you don't have to lose sleep over it.

FROM OUR BLOG

Join The Team!

NOW HIRING: Transaction Coordinator / Manager Independent Contractor | Kansas & Missouri | eXp Realty LLCRemote-Flexible | Per-Transaction Compensation THE PITCH Real estate is beautiful chaos. One minute you're negotiating repairs, the next you're talking someone off a ledge because the title

Just Launched: Kansas City Area Rent to Own Program

The Path to Homeownership Isn't the Same For Everyone. We’re excited to offer, through a partnership between Jana Jeffery and Berry-Rock Homes, a Rent-to-Own option for home buyers who want or need to take a less traditional path to homeownership or are interested in the flexibility Rent-to-Own affo

What is an Appraisal?

If you’re buying or selling a home, especially for the first time, the word appraisal can feel intimidating. It sounds official. It sounds final. And it often shows up late in the process when emotions are already running high. Let’s break it down in plain language. What a Home Appraisal Really Is A